10-K: Annual report pursuant to Section 13 and 15(d)

Published on March 8, 2019

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

☒ |

Annual Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended December 30, 2018

or

|

☐ |

Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to

Commission File Number: 0-21660

PAPA JOHN’S INTERNATIONAL, INC.

(Exact name of registrant as specified in its charter)

|

Delaware |

|

61-1203323 |

|

(State or other jurisdiction of |

|

(I.R.S. Employer |

|

incorporation or organization) |

|

Identification No.) |

|

2002 Papa John’s Boulevard |

|

|

|

Louisville, Kentucky |

|

40299-2367 |

|

(Address of principal executive offices) |

|

(Zip Code) |

(502) 261-7272

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

(Title of Each Class) |

|

(Name of each exchange on which registered) |

|

Common Stock, $0.01 par value |

|

The NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ☒ |

|

Accelerated filer ☐ |

|

Non-accelerated filer ☐ |

|

Smaller reporting company ☐ Emerging growth company ☐

|

If an emerging growth company, indicate by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

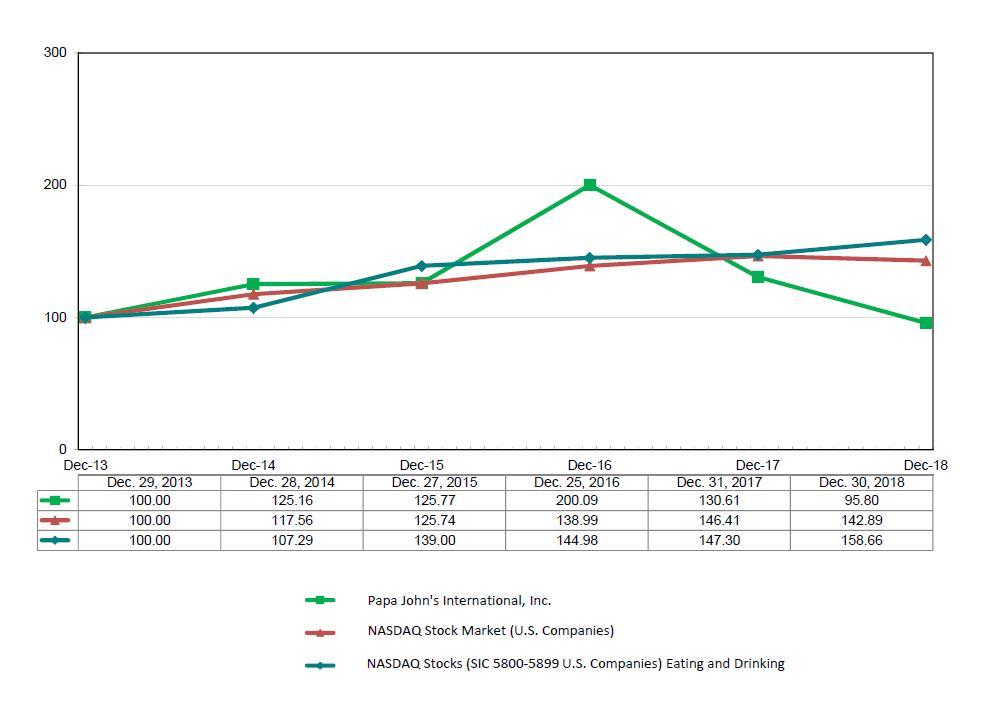

The aggregate market value of the common stock held by non-affiliates of the Registrant, computed by reference to the closing sale price on The NASDAQ Stock Market as of the last business day of the Registrant’s most recently completed second fiscal quarter, July 1, 2018, was $1,120,697,454.

As of March 4, 2019, there were 31,642,269 shares of the Registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of Part III of this annual report are incorporated by reference to the Registrant’s Proxy Statement for the Annual Meeting of Stockholders to be held April 30, 2019.

2

General

Papa John’s International, Inc., a Delaware corporation (referred to as the “Company”, “Papa John’s” or in the first person notations of “we”, “us” and “our”), operates and franchises pizza delivery and carryout restaurants and, in certain international markets, dine-in and delivery restaurants under the trademark “Papa John’s”. Papa John’s began operations in 1984. At December 30, 2018, there were 5,303 Papa John’s restaurants in operation, consisting of 645 Company-owned and 4,658 franchised restaurants operating domestically in all 50 states and in 46 countries and territories. Our Company-owned restaurants include 183 restaurants operated under three joint venture arrangements.

Papa John’s has defined four reportable segments: domestic Company-owned restaurants, North America commissaries (Quality Control Centers), North America franchising and international operations. North America is defined as the United States and Canada. Domestic is defined as the contiguous United States. International franchisees are defined as all franchise operations outside of the United States and Canada. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Note 22” of “Notes to Consolidated Financial Statements” for financial information about our segments.

All of our periodic and current reports filed with the Securities and Exchange Commission (the “SEC”) pursuant to Section 13(a) or 15(d) of the Securities and Exchange Act of 1934, as amended (the “Exchange Act”), are available, free of charge, through our website located at www.papajohns.com. These reports include our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to those reports. These reports are available through our website as soon as reasonably practicable after we electronically file them with the SEC. We also make available free of charge on our website our Corporate Governance Guidelines, Board Committee Charters, and our Code of Ethics, which applies to Papa John’s directors, officers and employees. Printed copies of such documents are also available free of charge upon written request to Investor Relations, Papa John’s International, Inc., P.O. Box 99900, Louisville, KY 40269-0900. The SEC maintains an internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC, including us, at www.sec.gov. The references to these website addresses do not constitute incorporation by reference of the information contained on the websites, which should not be considered part of this document.

We have experienced negative publicity and consumer sentiment as a result of statements by the Company’s founder and former spokesperson John H. Schnatter in late 2017 and in July 2018, which contributed to our negative sales results in 2018. Mr. Schnatter resigned as Chairman of the Board on July 11, 2018, the same day that the media reported certain controversial statements made by Mr. Schnatter. A Special Committee of the Board of Directors consisting of all of the independent directors (the “Special Committee”) was formed on July 15, 2018 to evaluate and take action with respect to all of the Company’s relationships and arrangements with Mr. Schnatter. In addition, on July 27, 2018, the Company announced that the Board’s Lead Independent Director, Olivia F. Kirtley, had been unanimously appointed by the Board of Directors to serve as Chairman of the Company’s Board of Directors. Following its formation, the Special Committee terminated Mr. Schnatter’s Founder Agreement, which defined his role in the Company, among other things, as advertising and brand spokesperson for the Company. The Special Committee, among other things, oversaw the previously announced external audit and investigation of all the Company’s existing processes, policies and systems related to diversity and inclusion, supplier and vendor engagement and Papa John’s culture, which is substantially complete. The Special Committee has delivered recommendations resulting from the audit to Company management, who will implement the recommendations, including initiatives and training regarding Diversity, Equity, and Inclusion. The Company is also implementing various branding and marketing initiatives, including a new advertising and marketing campaign.

In September 2018, the Company began a process to evaluate a wide range of strategic options with the goal of improving sales, maximizing value for all shareholders and serving the best interest of the Company’s stakeholders. As part of this strategic review, the Special Committee also engaged legal and financial advisors. After extensive discussions with a wide group of strategic and financial investors, the Special Committee concluded that an investment agreement with funds

3

affiliated with Starboard Value LP (together with its affiliates, “Starboard”) was in the best interest of shareholders. On February 3, 2019, the Company entered into a Securities Purchase Agreement (the “Securities Purchase Agreement”) with Starboard pursuant to which Starboard made a $200 million strategic investment in the Company’s newly designated Series B convertible preferred stock, par value $0.01 per share (the “Series B Preferred Stock”), with the option to make an additional $50 million investment in the Series B Preferred Stock through March 29, 2019. In addition, the Company has the right to offer up to 10,000 shares of Series B Preferred Stock to Papa John’s franchisees, on the same terms as to Starboard, provided such franchisees satisfy accredited investor and other requirements of the offering under securities laws.

The Company will use approximately half of the proceeds from the sale of the Series B Preferred Stock to reduce the outstanding principal amount under the Company’s unsecured revolving credit facility. The remaining proceeds are expected to be used to make investments in the business and for general corporate purposes.

In connection with Starboard’s investment, the Company expanded its Board of Directors to include two new independent directors, Jeffrey C. Smith, Chief Executive Officer of Starboard, who was appointed Chairman of the Board, and Anthony M. Sanfilippo, former Chairman and Chief Executive Officer of Pinnacle Entertainment, Inc. The Board of Directors believes Mr. Smith’s business expertise and new perspectives will help support the Company’s strategy to capitalize on its differentiated “BETTER INGREDIENTS. BETTER PIZZA.” market position and build a better pizza company for the benefit of its shareholders, team members, franchisees and customers. In addition, the Company’s President and Chief Executive Officer, Steve Ritchie, has been appointed to the Board. With the addition of the new directors, the Board currently is comprised of nine directors, seven of whom are independent.

Comparable Sales Trends. For the period from December 31, 2018 to January 31, 2019, system-wide North America comparable sales decreased 10.5% and system-wide International comparable sales were flat. The Company believes the disparity in North America and International comparable sales reflects the consumer sentiment challenges the brand has encountered in the United States. The Company is implementing various brand initiatives, including a new advertising and marketing campaign, in an effort to reverse the negative North America sales trend. However, the Company cannot predict whether or how long the negative sales trend will continue.

Special Charges. The Company also incurred significant costs (defined as “Special charges”) as a result of the above-mentioned recent events in the second half of 2018. We incurred $50.7 million of Special charges as follows:

|

· |

franchise royalty reductions of approximately $15.4 million for all North America franchisees, |

|

· |

reimaging costs at nearly all domestic restaurants and replacement or write off of certain branded assets totaling $5.8 million, |

|

· |

contribution of $10.0 million to the Papa John’s National Marketing Fund (“PJMF”), and |

|

· |

legal and professional fees, which amounted to $19.5 million, for various matters relating to the review of a wide range of strategic opportunities for the Company that culminated in the recent strategic investment in the Company by affiliates of Starboard, as well as a previously announced external culture audit and other activities overseen by the Special Committee. |

The Company estimates that these costs will amount to between $30 million and $50 million for 2019.

Following these events in 2018, we became a party to litigation, including class action securities litigation and litigation with Mr. Schnatter. See Item 1A. Risk Factors and “Note 19” to the “Consolidated Financial Statements” for additional information regarding these and other lawsuits.

Strategy

Early in 2018, we outlined five strategic priorities to improve upon the execution of the Company’s strategy, including:

|

· |

People: Focus on making people a priority with advanced career opportunities and more efficient restaurant procedures to support improved recruitment and retention. |

|

· |

Brand differentiation messaging: Develop improved marketing messaging that highlights our quality products and ingredients. |

4

|

· |

Value perception: Provide everyday accessible value to consumers. |

|

· |

Technological advancements: Promote technological advancements with enhanced data and analytics capabilities. |

|

· |

Restaurant unit economics: Invest further in our restaurants to operate more efficiently while improving the customer experience. |

We believe investments in these areas will provide the enhanced focus and support necessary to achieve our goal to build brand loyalty over the long-term by delivering on our “BETTER INGREDIENTS. BETTER PIZZA.” promise. Despite our recent brand challenges, we believe we are recognized as a trusted brand and quality leader in the domestic pizza category, and we believe focusing on these areas will enable us to build our brand on a global basis and increase sales and global units.

High-Quality Menu Offerings. Our menu strategy focuses on the quality of our ingredients. Domestic Papa John’s restaurants offer high-quality pizza along with side items, including breadsticks, cheesesticks, chicken poppers and wings, dessert items and canned or bottled beverages. Papa John’s original crust pizza is prepared using fresh dough (never frozen). Papa John’s pizzas are made from a proprietary blend of wheat flour; real cheese made from mozzarella; fresh-packed pizza sauce made from vine-ripened tomatoes (not from concentrate) and a proprietary mix of savory spices; and a choice of high-quality meat and vegetable toppings. Our original and pan dough crust pizza is delivered with a container of our special garlic sauce and a pepperoncini pepper. In addition to our fresh dough pizzas, we offer a par-baked thin crust and a gluten free crust. Each is served with a pepperoncini pepper. We have a continuing “clean label” initiative to remove unwanted ingredients from our product offerings over the next few years, such as synthetic colors, artificial flavors and preservatives.

We also offer limited-time pizzas on a regular basis and expect to expand these offerings in 2019. We also test new product offerings both domestically and internationally. The new products can become a part of the permanent menu if they meet certain internally established guidelines.

All ingredients and toppings can be purchased by our Company-owned and franchised restaurants from our North American Quality Control Center (“QC Center”) system, which delivers to individual restaurants twice weekly. To ensure consistent food quality, each domestic franchisee is required to purchase dough and pizza sauce from our QC Centers and to purchase all other supplies from our QC Centers or other approved suppliers. Internationally, the menu may be more diverse than in our domestic operations to meet local tastes and customs. Most QC Centers outside the U.S. are operated by franchisees pursuant to license agreements or by other third parties. The Company currently operates only one international QC Center, which is in the United Kingdom (“UK”). Our China QC Center was sold to a franchisee in 2018 and our QC Center in Mexico City was sold to a franchisee in early 2019. We provide significant assistance to licensed QC Centers in sourcing approved quality suppliers. All QC Centers are required to meet food safety and quality standards and to be in compliance with all applicable laws.

Efficient Operating System. We believe our operating and distribution systems, restaurant layout and designated delivery areas result in improved food quality and customer service as well as lower restaurant operating costs. Our QC Center system takes advantage of volume purchasing of food and supplies. The QC Center system also provides consistency and efficiencies of scale in fresh dough production. This eliminates the need for each restaurant to order food from multiple vendors and commit substantial labor and other resources to dough preparation.

Commitment to Team Member Training and Development. We are committed to the development and motivation of our team members through training programs, including our leadership development programs, Diversity, Equity and Inclusion initiatives and training, incentive and recognition programs and opportunities for advancement. Team member training programs are conducted for Company-owned restaurant team members, and operational training is offered to our franchisees. We offer performance-based financial incentives to corporate team members and restaurant managers.

Marketing. Our branding efforts seek to showcase the values of the Company and its team members. We evaluate marketing investments with respect to their ability to activate and accelerate positive consumer sentiment, utilizing campaigns that spotlight the Company’s differentiated focus on quality, better ingredients and better pizza.

5

Our domestic marketing strategy consists of both national and local components. Our national strategy includes national advertising via television, print, direct mail, digital, mobile marketing and social media channels. Our digital marketing activities have increased significantly over the past several years in response to increasing customer use of online and mobile web technology. Local advertising programs include television, radio, print, direct mail, store-to-door flyers, digital, mobile marketing and local social media channels. See “Marketing Programs” below, which describes more local marketing programs.

In international markets, our marketing focuses on reaching customers who live or work within a small radius of a Papa John’s restaurant. Our international markets use a combination of advertising strategies, including television, radio, print, digital, mobile marketing and local social media depending on the size of the local market.

Technology. We use technology to deliver a better customer experience, focusing on key strategies that offer benefits to the customer as well as advancing our objectives of higher customer lifetime value and deeper brand affinity.

Our technology initiatives build on our past milestones, which include the introduction of digital ordering across all our U.S. delivery restaurants in 2001 and the launch of a domestic digital rewards program in 2010. In 2018, over 60% of domestic sales were placed through digital channels. Technology investments have included enhanced digital ordering and expanded mobile app capabilities. As we continue to enhance our digital capabilities, we have focused on technology investments that allow us to use data to target marketing programs to individual customers as well as customer segments. In late 2018, we relaunched our digital rewards program with enhanced targeted marketing capabilities.

Franchise System. We are committed to developing and maintaining a strong franchise system by attracting experienced operators, supporting them to expand and grow their business and monitoring their compliance with our high standards. We seek to attract and retain franchisees with experience in restaurant or retail operations and with the financial resources and management capability to open single or multiple locations. While each Papa John’s franchisee manages and operates its own restaurants and business, we devote significant resources to providing franchisees with assistance in restaurant operations, training, marketing, site selection and restaurant design.

Our strategy for global franchise unit growth focuses on our sound unit economics model. We strive to eliminate barriers to expansion in existing international markets, and identify new market opportunities. Our growth strategy varies based on the maturity and penetration of the market and other factors in specific domestic and international markets, with overall unit growth expected to come increasingly from international markets.

Restaurant Sales and Investment Costs

We are committed to maintaining sound restaurant unit economics. In 2018, the 637 domestic Company-owned restaurants included in the full year’s comparable restaurant base generated average annual unit sales of $1.07 million. Our North American franchise restaurants, which included 2,396 restaurants in the full year’s comparable base for 2018, generated average annual unit sales of $840,000. Average annual unit sales for North American franchise restaurants are lower than those of Company-owned restaurants as a higher percentage of our Company-owned restaurants are located in more heavily penetrated markets.

With only a few exceptions, domestic restaurants do not offer dine-in service, which reduces our restaurant capital investment. The average cash investment for the six domestic traditional Company-owned restaurants opened during 2018, exclusive of land, was approximately $345,000 per unit, compared to the $354,000 investment for the 12 domestic traditional units opened in 2017, excluding tenant allowances that we received. In recent years, we have experienced an increase in the cost of our new restaurants primarily as a result of building larger units and incurring higher costs of certain equipment as a result of technology enhancements and increased costs to comply with applicable regulations.

We define a “traditional” domestic Papa John’s restaurant as a delivery and carryout unit that services a defined trade area. We consider the location of a traditional restaurant to be important and therefore devote significant resources to the investigation and evaluation of potential sites. The site selection process includes a review of trade area demographics, target population density and competitive factors. A member of our development team inspects each potential domestic Company-owned restaurant location and substantially all franchised restaurant locations before a site is approved. Papa

6

John’s restaurants are typically located in strip shopping centers or freestanding buildings that provide visibility, curb appeal and accessibility. Our restaurant design can be configured to fit a wide variety of building shapes and sizes, which increases the number of suitable locations for our Company-owned and franchised restaurants. A typical traditional domestic Papa John’s restaurant averages 1,100 to 1,500 square feet with visible exterior signage.

“Non-traditional” Papa John’s restaurants generally do not provide delivery service but rather provide walk-up or carryout service to a captive customer group within a designated facility, such as a food court at an airport, university or military base or an event-driven service at facilities such as sports stadiums or entertainment venues. Non-traditional units are designed to fit the unique requirements of the venue and may not offer the full range of menu items available in our traditional restaurants.

As of December 30, 2018, all of our international restaurants are franchised. Generally, our international Papa John’s restaurants are slightly smaller than our domestic restaurants and average between 900 and 1,400 square feet; however, in order to meet certain local customer preferences, some international restaurants have been opened in larger spaces to accommodate both dine-in and restaurant-based delivery service, ranging from 35 to 140 seats.

Development

At December 30, 2018, there were 5,303 Papa John’s restaurants operating in all 50 states and in 46 international countries and territories, as follows:

|

|

Domestic Company-owned |

Franchised North America |

Total North America |

International |

System-wide |

|

|

|

|

|

|

|

|

Beginning - December 31, 2017 |

708 |

2,733 |

3,441 |

1,758 |

5,199 |

|

Opened |

6 |

83 |

89 |

304 |

393 |

|

Closed |

(7) |

(186) |

(193) |

(96) |

(289) |

|

Acquired |

- |

62 |

62 |

34 |

96 |

|

Sold |

(62) |

- |

(62) |

(34) |

(96) |

|

Ending - December 30, 2018 |

645 |

2,692 |

3,337 |

1,966 |

5,303 |

Although most of our domestic Company-owned markets are well-penetrated, our Company-owned growth strategy is to continue to open domestic restaurants in existing markets as appropriate, thereby increasing consumer awareness and enabling us to take advantage of operational and marketing efficiencies. Our experience in developing markets indicates that market penetration through the opening of multiple restaurants in a particular market results in increased average restaurant sales in that market over time. We have co-developed domestic markets with some franchisees or divided markets among franchisees and will continue to utilize market co-development in the future, where appropriate.

Of the total 3,337 North American restaurants open as of December 30, 2018, 645 units, or approximately 19%, were Company-owned (including 183 restaurants owned in joint venture arrangements with franchisees in which the Company has a majority ownership position and control). Operating Company-owned restaurants allows us to improve operations, training, marketing and quality standards for the benefit of the entire system. From time to time, we evaluate the purchase or sale of units or markets, which could change the percentage of Company-owned units. During 2018, we sold 62 restaurants located in Denver, Colorado and in Minnesota, in each case to a franchise group.

All of the 1,966 international restaurants are franchised after the 2018 sale of the Company’s 34 restaurants located in Beijing and North China.

QC Center System and Supply Chain Management

Our North American QC Center system currently comprises 11 full-service regional production and distribution centers in the U.S which supply pizza sauce, dough, food products, paper products, smallwares and cleaning supplies twice weekly to each traditional restaurant served. Additionally, we have one QC Center in Canada, which produces and distributes fresh dough. This system enables us to monitor and control product quality and consistency while lowering food and other

7

costs. We evaluate the QC Center system capacity in relation to existing restaurants’ volumes and planned restaurant growth, and facilities are developed or upgraded as operational or economic conditions warrant.

In addition, we currently own a full-service international QC Center in Milton Keynes, United Kingdom. Other international QC Centers are licensed to franchisees or non-franchisee third parties and are generally located in the markets where our franchisees have restaurants.

We set quality standards for all products used in Papa John’s restaurants and designate approved outside suppliers of food and paper products that meet our quality standards. To ensure product quality and consistency, all domestic Papa John’s restaurants are required to purchase pizza sauce and dough from QC Centers. Franchisees may purchase other goods directly from our QC Centers or other approved suppliers. National purchasing agreements with most of our suppliers generally result in volume discounts to us, allowing us to sell products to our restaurants at prices we believe are below those generally available to other restaurants. Within our North American QC Center system, products are primarily distributed to restaurants by leased refrigerated trucks operated by us.

Marketing Programs

Our local restaurant-level marketing programs target potential customers within the delivery area of each restaurant through the use of local television, radio, print materials, targeted direct mail, store-to-door flyers, digital display advertising, email marketing, text messages and local social media. Local marketing efforts also include a variety of community-oriented activities within schools, sports venues and other organizations supported with some of the same advertising vehicles mentioned above. We recently began working with delivery aggregators to reach other customer channels and also enhanced our domestic loyalty program at the end of 2018.

Domestic Company-owned and franchised Papa John’s restaurants within a defined market may be required to join an area advertising cooperative (“Co-op”). Each member restaurant contributes a percentage of sales to the Co-op for market-wide programs, such as television, radio, digital and print advertising, and sports sponsorships. The rate of contribution and uses of the monies collected are determined by a majority vote of the Co-op’s members. The contribution rate for Co-ops generally may not be below 2% of sales without approval from Papa John’s.

The restaurant-level and Co-op marketing efforts are supported by media, print, digital and electronic advertising materials that are produced by Papa John’s Marketing Fund, Inc. (“PJMF”). PJMF is an unconsolidated nonstock corporation designed to operate at break-even for the purpose of designing and administering advertising and promotional programs for all participating domestic restaurants. PJMF produces and buys air time for Papa John’s national television commercials, and advertises the Company’s products through digital media including banner advertising, paid search-engine advertising, mobile marketing, social media advertising and marketing, text messaging, and emailing. It also engages in other brand-building activities, such as consumer research and public relations activities. Domestic Company-owned and franchised Papa John’s restaurants are required to contribute a certain minimum percentage of sales to PJMF. The contribution rate to PJMF can be set at up to 3% of sales, if approved by the governing board of PJMF, and beyond that level if approved by a supermajority of domestic restaurants. The domestic franchise system approved a new contribution rate of 4.50% effective in the fourth quarter of 2017. The rate increased an additional 0.25% to 4.75% effective at the beginning of 2019.

Our proprietary domestic digital ordering platform allows customers to order online, including “plan ahead ordering,” Apple TV ordering and Spanish-language ordering capability. Digital payment platforms include VISA Checkout, PayPal, and Venmo PayShare. We provide enhanced mobile ordering for our customers, including Papa John’s iPhone® and Android® applications. Our Papa Rewards® program is a customer loyalty program designed to increase loyalty and frequency; we offer this program domestically, in the UK, and in several international markets. We receive a percentage-based fee from North American franchisees for online sales, in addition to royalties, to defray development and operating costs associated with our digital ordering platform. We believe continued innovation and investment in the design and functionality of our online and mobile platforms is critical to the success of our brand.

Our domestic restaurants offer customers the opportunity to purchase reloadable gift cards, sold as either a plastic gift card purchased in our restaurants, or an online digital card. Gift cards are sold to customers on our website, through third-party

8

retailers, and in bulk to business entities and organizations. We continue to explore other gift card distribution opportunities. Gift cards may be redeemed for delivery, carryout, and digital orders and are accepted at all Papa John’s traditional domestic restaurants.

We provide both Company-owned and franchised restaurants with pre-approved marketing materials and catalogs for the purchase of promotional items. We also provide direct marketing services to Company-owned and domestic franchised restaurants using customer information gathered by our proprietary point-of-sale technology (see “Company Operations —North America Point-of-Sale Technology”). In addition, we provide database tools, templates and training for operators to facilitate local email marketing and text messaging through our approved tools.

In international markets, our marketing focuses on customers who live or work within a small radius of a Papa John’s restaurant. Certain markets can effectively use television and radio as part of their marketing strategies. The majority of the marketing efforts include using print materials such as flyers, newspaper inserts, in-store marketing materials, and to a growing extent, digital marketing such as display, search engine marketing, social media, mobile marketing, email, and text messaging. Local marketing efforts, such as sponsoring or participating in community events, sporting events and school programs, are also used to build customer awareness.

Company Operations

Domestic Restaurant Personnel. A typical Papa John’s Company-owned domestic restaurant employs a restaurant manager and approximately 20 to 25 hourly team members, many of whom work part-time. The manager is responsible for the day-to-day operation of the restaurant and maintaining Company-established operating standards. We seek to hire experienced restaurant managers and staff and provide comprehensive training programs in areas such as operations and managerial skills. We also employ directors of operations who are responsible for overseeing an average of seven Company-owned restaurants. Senior management and corporate staff also support the field teams in many areas, including, but not limited to, quality assurance, food safety, training, marketing and technology. We seek to motivate and retain personnel by providing opportunities for advancement and performance-based financial incentives.

Training and Education. We believe training is very important to delivering consistent operational execution, and we create tools and materials for the operational training and development of both corporate and franchise team members. Operations personnel complete our management training program and ongoing development programs, including multi-unit training, in which instruction is given on all aspects of our systems and operations.

North America Point-of-Sale Technology. Our proprietary point-of-sale technology, “FOCUS”, is in place in all North America traditional Papa John’s restaurants. We believe this technology facilitates fast and accurate order-taking and pricing, and allows the restaurant manager to better monitor and control food and labor costs, including food inventory management and order placement from QC Centers. The system allows us to obtain restaurant operating information, providing us with timely access to sales and customer information. The FOCUS system is also integrated with our digital ordering solutions in all North American traditional Papa John’s restaurants.

Domestic Hours of Operation. Our domestic restaurants are open seven days a week, typically from 11:00 a.m. to 12:30 a.m. Monday through Thursday, 11:00 a.m. to 1:30 a.m. on Friday and Saturday and 12:00 noon to 11:30 p.m. on Sunday. Carryout hours are generally more limited for late night service, for security purposes.

Franchise Program

General. We continue to attract qualified and experienced franchisees, whom we consider to be a vital part of our system’s continued growth. We believe our relationship with our franchisees is fundamental to the performance of our brand and we strive to maintain a collaborative relationship with our franchisees. As of December 30, 2018, there were 4,658 franchised Papa John’s restaurants operating in all 50 states and 46 countries and territories. During 2018, our franchisees opened an additional 387 (83 North America and 304 internationally) restaurants, which includes the opening of Papa John’s restaurants in three new countries: the Bahamas, Kazakhstan and Kyrgyzstan. As of December 30, 2018, we have development agreements with our franchisees for approximately 130 additional North America restaurants, the majority of which are committed to open over the next two years, and agreements for approximately 900 additional international franchised restaurants, the majority of which are scheduled to open over the next six years. There can be no assurance that

9

all of these restaurants will be opened or that the development schedules set forth in the development agreements will be achieved.

Approval. Franchisees are approved on the basis of the applicant’s business background, restaurant operating experience and financial resources. We seek franchisees to enter into development agreements for single or multiple restaurants. We require each franchisee to complete our training program or to hire a full-time operator who completes the training and has either an equity interest or the right to acquire an equity interest in the franchise operation. For most non-traditional operations and for operations outside the United States, we will allow an approved operator bonus plan to substitute for the equity interest.

North America Development and Franchise Agreements. We enter into development agreements with our franchisees in North America for the opening of a specified number of restaurants within a defined period of time and specified geographic area. Our standard domestic development agreement includes a fee of $25,000 before consideration of any incentives. The franchise agreement is generally executed once a franchisee secures a location. Our current standard franchise agreement requires the franchisee to pay a royalty fee of 5% of sales, and the majority of our existing franchised restaurants have a 5% contractual royalty rate in effect. Incentives offered from time to time, including new store incentives, will reduce the actual royalty rate paid. Incentives in effect in the later part of 2018 to support the franchise system included a royalty reduction of 2% and 1% for the third and fourth quarters, respectively.

Over the past several years, we have offered various development incentive programs for domestic franchisees to accelerate unit openings. Such incentives included the following for 2018 traditional openings: (1) waiver of the standard one-time $25,000 franchise fee if the unit opens on time in accordance with the agreed-upon development schedule, or a reduced fee of $5,000 if the unit opens late; (2) the waiver of some or all of the 5% royalty fee for a period of time; (3) a credit for new store equipment; and (4) a credit to be applied toward a future food purchase, under certain circumstances. We believe development incentive programs have accelerated unit openings.

Substantially all existing franchise agreements have an initial 10-year term with a 10-year renewal option. We have the right to terminate a franchise agreement for a variety of reasons, including a franchisee’s failure to make payments when due or failure to adhere to our operational policies and standards. Many state franchise laws limit our ability as a franchisor to terminate or refuse to renew a franchise.

We provide assistance to Papa John’s franchisees in selecting sites, developing restaurants and evaluating the physical specifications for typical restaurants. We provide layout and design services and recommendations for subcontractors, signage installers and telephone systems to Papa John’s franchisees. Our franchisees can purchase complete new store equipment packages through an approved third-party supplier. We sell replacement smallwares and related items to our franchisees. Each franchisee is responsible for selecting the location for its restaurants, but must obtain our approval of the restaurant design and location based on traffic accessibility and visibility of the site and targeted demographic factors, including population density, income, age and traffic.

Domestic Franchise Support Initiatives. In 2018, we have increased our franchise support initiatives in light of the current sales pressures by providing additional royalty reductions of 2% and 1% in the third and fourth quarters, respectively. Historically, discretionary support initiatives to our domestic franchisees, included the following:

|

· |

Performance-based incentives; |

|

· |

Targeted royalty relief and local marketing support to assist certain identified franchisees or markets; |

|

· |

Restaurant opening incentives; and |

|

· |

Reduced-cost direct mail campaigns from Preferred Marketing Solutions (“Preferred”), our wholly owned print and promotions subsidiary. |

In 2019, we plan to offer some or all of these domestic franchise support initiatives, with a particular focus of providing assistance to franchisees in emerging and/or high cost markets.

International Development and Franchise Agreements. We define “international” as all markets outside the United States and Canada. In international markets, we have either a development agreement or a master franchise agreement with a

10

franchisee for the opening of a specified number of restaurants within a defined period of time and specified geographic area. Under a master franchise agreement, the franchisee has the right to sub-franchise a portion of the development to one or more sub-franchisees approved by us. Under our current standard international development or master franchise agreement, the franchisee is required to pay total fees of $25,000 per restaurant: $5,000 at the time of signing the agreement and $20,000 when the restaurant opens or on the agreed-upon development date, whichever comes first. Additionally, under our current standard master franchise agreement, the master franchisee is required to pay $15,000 for each sub-franchised restaurant — $5,000 at the time of signing the agreement and $10,000 when the restaurant opens or on the agreed-upon development date, whichever comes first.

Our current standard international master franchise and development agreements provide for payment to us of a royalty fee of 5% of sales. For international markets with sub-franchise agreements, the effective sub-franchise royalty received by the Company is generally 3% of sales and the master franchisee generally receives a royalty of 2% of sales. The remaining terms applicable to the operation of individual restaurants are substantially equivalent to the terms of our domestic franchise agreement. Development agreements will be negotiated at other-than-standard terms for fees and royalties, and we may offer various development and royalty incentives to help drive net unit growth and results.

Non-traditional Restaurant Development. We had 247 non-traditional domestic restaurants at December 30, 2018. Non-traditional restaurants generally cover venues or areas not originally targeted for traditional unit development, and our franchised non-traditional restaurants have terms differing from the standard agreements.

Franchisee Loans. Selected domestic and international franchisees have borrowed funds from us, principally for the purchase of restaurants from us or other franchisees or for construction and development of new restaurants. Loans made to franchisees can bear interest at fixed or floating rates and in most cases are secured by the fixtures, equipment and signage of the restaurant and/or are guaranteed by the franchise owners. At December 30, 2018, net loans outstanding totaled $28.8 million. See “Note 13” of “Notes to Consolidated Financial Statements” for additional information.

Domestic Franchise Training and Support. Our domestic field support structure consists of franchise business directors who are responsible for serving an average of 165 franchised units each. Our franchise business directors maintain open communication with the franchise community, relaying operating and marketing information and new initiatives between franchisees and us.

Every franchisee is required to have a principal operator approved by us who satisfactorily completes our required training program. Principal operators for traditional restaurants are required to devote their full business time and efforts to the operation of the franchisee’s traditional restaurants. Each franchised restaurant manager is also required to complete our Company-certified management operations training program and we monitor ongoing compliance with training. Multi-unit franchisees are encouraged to appoint training store general managers or hire a full-time training coordinator certified to deliver Company-approved operational training programs.

International Franchise Operations Support. We employ or contract with international business directors who are responsible for supporting one or more franchisees. The international business directors usually report to regional vice presidents. Senior management and corporate staff also support the international field teams in many areas, including, but not limited to, food safety, quality assurance, marketing, technology, operations training and financial analysis.

Franchise Operations. All franchisees are required to operate their Papa John’s restaurants in compliance with our policies, standards and specifications, including matters such as menu items, ingredients, and restaurant design. Franchisees have full discretion in human resource practices, and generally have full discretion to determine the prices to be charged to customers, but we generally have the authority to set maximum price points for nationally advertised promotions.

Franchise Advisory Council. We have a franchise advisory council that consists of Company and franchisee representatives of domestic restaurants. We also have a franchise advisory council in the United Kingdom. The various councils and subcommittees hold regular meetings to discuss new product and marketing ideas, operations, growth and other business issues. Certain domestic franchisees have also formed an independent franchise association for the purpose of communicating and addressing issues, needs and opportunities among its members.

11

We currently communicate with, and receive input from, our franchisees in several forms, including through the various councils, annual operations conferences, system communications, national conference calls, various regional meetings conducted with franchisees throughout the year and ongoing communications from franchise business directors and international business directors in the field. Monthly webcasts are also conducted by the Company to discuss current operational, marketing and other issues affecting the domestic franchisees’ business. We are committed to communicating with our franchisees and receiving input from them.

Industry and Competition

The United States Quick Service Restaurant pizza (“QSR Pizza”) industry is mature and highly competitive with respect to price, service, location, food quality, customer loyalty programs and product innovation. There are well-established competitors with substantially greater financial and other resources than Papa John’s. The category is largely fragmented and competitors include international, national and regional chains, as well as a large number of local independent pizza operators, any of which can utilize a growing number of food delivery services. Some of our competitors have been in existence for substantially longer periods than Papa John’s and can have higher levels of restaurant penetration and stronger, more developed brand awareness in markets where we compete. According to industry sources, domestic QSR Pizza category sales, which includes dine-in, carry out and delivery, totaled approximately $37 billion in 2018, or an increase of 2.0% from the prior year. Competition from delivery aggregators and other food delivery concepts continues to increase both domestically and internationally.

With respect to the sale of franchises, we compete with many franchisors of restaurants and other business concepts. There is also active competition for management personnel, drivers and hourly team members, and attractive commercial real estate sites suitable for Papa John’s restaurants.

We, along with our franchisees, are subject to various federal, state, local and international laws affecting the operation of our respective businesses, including laws and regulations related to the preparation and sale of food, including food safety and menu labeling. Each Papa John’s restaurant is subject to licensing and regulation by a number of governmental authorities, which include zoning, health, safety, sanitation, building and fire agencies in the state or municipality in which the restaurant is located. Difficulties in obtaining, or the failure to obtain, required licenses or approvals could delay or prevent the opening of a new restaurant in a particular area. Our QC Centers are licensed and subject to regulation by state and local health and fire codes, and the operation of our trucks is subject to federal and state transportation regulations. We are also subject to federal and state environmental regulations. In addition, our domestic operations are subject to various federal and state laws governing such matters as minimum wage requirements, benefits, working conditions, citizenship requirements, and overtime.

We are subject to Federal Trade Commission (“FTC”) regulation and various state laws regulating the offer and sale of franchises. The laws of several states also regulate substantive aspects of the franchisor-franchisee relationship. The FTC requires us to furnish to prospective franchisees a franchise disclosure document containing prescribed information. State laws that regulate the franchisor-franchisee relationship presently exist in a significant number of states, and bills have been introduced in Congress from time to time that would provide for federal regulation of the U.S. franchisor-franchisee relationship in certain respects if such bills were enacted. State laws often limit, among other things, the duration and scope of non-competition provisions and the ability of a franchisor to terminate or refuse to renew a franchise. Some foreign countries also have disclosure requirements and other laws regulating franchising and the franchisor-franchisee relationship. National, state and local government regulations or initiatives, including health care legislation, “living wage,” or other current or proposed regulations, and increases in minimum wage rates affect Papa John’s as well as others within the restaurant industry. As we expand internationally, we are also subject to applicable laws in each jurisdiction.

We are subject to laws and regulations that require us to disclose calorie content and other specific content of our food, including fat, trans fat, and salt content. A provision of the Patient Protection and Affordable Care Act of 2010 (ACA) requires us and many restaurant companies to disclose calorie information on restaurant menus. The Food and Drug Administration issued final rules to implement this provision, which require restaurants to post the number of calories for most items on menus or menu boards and to make available certain other nutritional information. Government regulation

12

of nutrition disclosure could result in increased costs of compliance and could also impact consumer habits in a way that adversely impacts sales at our restaurants. For further information regarding governmental regulation, see Item 1A. Risk Factors.

Trademarks, Copyrights and Domain Names

Our intellectual property rights are a significant part of our business. We have registered and continue to maintain federal registrations through the United States Patent and Trademark Office (the “USPTO”) for the marks PAPA JOHN’S, PIZZA PAPA JOHN’S & Design (our logo), BETTER INGREDIENTS. BETTER PIZZA., PIZZA PAPA JOHN’S BETTER INGREDIENTS. BETTER PIZZA., PIZZA PAPA JOHN’S BETTER INGREDIENTS. BETTER PIZZA. & Design, and PAPA REWARDS. We also own federal registrations through the USPTO for several ancillary marks, principally advertising slogans. Moreover, we have registrations for and/or have applied for PIZZA PAPA JOHN’S & Design in more than 100 foreign countries and the European Community, in addition to international registrations for PAPA JOHN’S and PIZZA PAPA JOHN’S BETTER INGREDIENTS. BETTER PIZZA. & Design in various foreign countries. From time to time, we are made aware of the use by other persons in certain geographical areas of names and marks that are the same as or substantially similar to our marks. It is our policy to pursue registration of our marks whenever possible and to vigorously oppose any infringement of our marks.

We hold copyrights in authored works used in our business, including advertisements, packaging, training, website, and promotional materials. In addition, we have registered and maintain Internet domain names, including “papajohns.com,” and approximately 83 country code domains patterned as papajohns.cc, or a close variation thereof, with “.cc” representing a specific country code.

Employees

As of December 30, 2018, we employed approximately 18,000 persons, of whom approximately 15,400 were restaurant team members, approximately 700 were restaurant management personnel, approximately 700 were corporate personnel and approximately 1,200 were QC Center and Preferred personnel. Most restaurant team members work part-time and are paid on an hourly basis. None of our team members are covered by a collective bargaining agreement. We consider our team member relations to be good.

We are subject to risks that could have a negative effect on our business, financial condition and results of operations. These risks could cause actual operating results to differ from those expressed in certain “forward looking statements” contained in this Form 10-K as well as in other Company communications. Before you invest in our securities, you should carefully consider the following risk factors together with all other information included in this Form 10-K and our other publicly filed documents.

We have recently experienced negative publicity and consumer sentiment as a result of statements by the Company’s founder and former spokesperson, John H. Schnatter, which may continue to negatively impact our results of operations.

In July 2018, the Company was the subject of significant negative media reports as a result of certain statements by Mr. Schnatter, who resigned as Chairman of the Board on July 11, 2018. The negative media continued throughout the third quarter of 2018, and the resultant negative consumer sentiment continued throughout the remainder of the 2018 fiscal year.

As a result of the recent negative publicity and consumer sentiment, the Company has experienced a decline in sales and operating profits. This decline may continue if the negative consumer sentiment toward the Company continues or worsens. If Mr. Schnatter makes further statements that create controversy or harm the Company’s reputation, it may take longer for our sales and consumer perception of our brand to improve.

13

We will incur costs related to addressing and remediating the impact of recent negative publicity surrounding our brand as a result of John H. Schnatter, which will adversely impact our financial performance.

In connection with the controversy surrounding Mr. Schnatter, a Special Committee of the Board of Directors, consisting of all of the independent directors, was formed to evaluate and take action with respect to all of the Company’s relationships and arrangements with Mr. Schnatter. Following its formation, the Special Committee terminated Mr. Schnatter’s Founder Agreement, which defined his role in the Company, among other things, as advertising and brand spokesperson for the Company.

In connection with these and other actions, the Company has incurred and expects to continue to incur significant non-recurring costs in 2019, including costs related to branding initiatives, marketing and advertising expenses and increased professional fees. In addition, the Company materially increased its franchisee financial assistance in 2018 in an effort to mitigate store closings, and expects to continue some additional level of assistance in 2019. These costs and any additional costs we may incur to support these initiatives are expected to adversely affect our profitability and financial performance. There is no guarantee that our actions will be effective in attracting customers back to our restaurants and mitigating negative sales trends.

The recent negative publicity has had and may continue to have a negative impact on our business, and may have a long-term effect on our relationships with our customers, partners and franchisees.

Our business and reputation has been negatively affected by the recent negative publicity resulting from Mr. Schnatter’s statements. If we are unable to rebuild the trust of our customers, franchisees, business partners and suppliers, and if further negative publicity continues, we could experience a substantial negative impact on our business. We have experienced claims and litigation as a consequence of these matters, including a shareholder class action in connection with a decline in our stock price and litigation with Mr. Schnatter. Related legal expenses of defending these claims have negatively impacted our operating results. Continuing higher legal fees, potential new claims, liabilities from existing cases and continuing negative publicity could continue to have a negative impact on operating results.

We have experienced declining sales, and we cannot assure that we will be able to halt or reverse the decline.

Our system-wide North America and International comparable sales declined on a year-over-year basis in 2018. The Company’s revenues and profitability growth depend on the ability to increase comparable restaurant sales, and it is uncertain whether this will occur or could take longer than expected.

Our Board of Directors has adopted a limited duration stockholder rights agreement, which could delay or discourage a merger, tender offer, or assumption of control of the Company not approved by our Board of Directors.

On July 22, 2018, the Board of Directors approved the adoption of a limited duration stockholder rights plan (the “Rights Plan”) with an expiration date of July 22, 2019 and an ownership trigger threshold of 15% (with a threshold of 31% applied to John H. Schnatter, together with his affiliates and family members). In connection with the Rights Plan, the Board of Directors authorized and declared a dividend to stockholders of record at the close of business on August 2, 2018 of one preferred share purchase right (a “Right”) for each outstanding share of common stock of the Company. Upon certain triggering events, each Right entitles the holder to purchase from the Company one one-thousandth (subject to adjustment) of one share of Series A Junior Participating Preferred Stock, $0.01 par value per share (“Preferred Stock”) of the Company at an exercise price of $250.00 (the “Exercise Price”) per one one-thousandth of a share of Preferred Stock. In addition, if a person or group acquires beneficial ownership of 15% or more of the Company’s common stock (or in the case of Mr. Schnatter, 31% or more, and in the case of funds affiliated with Starboard Value LP, additional shares in excess of those issuable upon conversion of their Series B Convertible Preferred Stock) without prior board approval, each holder of a Right (other than the acquiring person or group whose Rights will become void) will have the right to purchase, upon payment of the Exercise Price and in accordance with the terms of the Rights Plan, a number of shares of the Company’s common stock having a market value of twice the Exercise Price. On March 5, 2019, the Board of Directors extended the term of the Rights Plan to March 6, 2022, increased the ownership trigger threshold at which a person becomes an acquiring person from 15% to 20%, except as set forth above, removed the “acting in concert” provision in response to stockholder feedback, and included a qualifying offer provision as set forth in the Rights Plan.

14

The Rights Plan is intended to enable all of our stockholders to realize the full potential value of their investment in the Company and to protect the interests of the Company and its stockholders by reducing the likelihood that any person or group gains control of the Company through open market accumulation or other tactics without paying an appropriate control premium. The Rights Plan could render more difficult, or discourage, a merger, tender offer, or assumption of control of the Company that is not approved by our Board of Directors. The Rights Plan, however, should not interfere with any merger, tender or exchange offer or other business combination approved by our Board of Directors. In addition, the Rights Plan does not prevent our Board of Directors from considering any offer that it considers to be in the best interest of the Company’s stockholders.

Our profitability may suffer as a result of intense competition in our industry.

The QSR Pizza industry is mature and highly competitive. Competition is based on price, service, location, food quality, brand recognition and loyalty, product innovation, effectiveness of marketing and promotional activity, use of technology, and the ability to identify and satisfy consumer preferences. We may need to reduce the prices for some of our products to respond to competitive and customer pressures, which may adversely affect our profitability. When commodity and other costs increase, we may be limited in our ability to increase prices. With the significant level of competition and the pace of innovation, we may be required to increase investment spending in several areas, particularly marketing and technology, which can decrease profitability.

In addition to competition with our larger and more established competitors, we face competition from new competitors such as fast casual pizza concepts. We also face competitive pressures from an array of food delivery concepts and aggregators delivering for quick service or dine in restaurants, using new delivery technologies, some of which may have more effective marketing. The emergence or growth of new competitors, in the pizza category or in the food service industry generally, may make it difficult for us to maintain or increase our market share and could negatively impact our sales and our system-wide restaurant operations. We also face increasing competition from other home delivery services and grocery stores that offer an increasing variety of prepped or prepared meals in response to consumer demand. As a result, our sales can be directly and negatively impacted by actions of our competitors, the emergence or growth of new competitors, consumer sentiment or other factors outside our control.

One of our competitive strengths is our “BETTER INGREDIENTS. BETTER PIZZA.” brand promise. This means we may use ingredients that cost more than the ingredients some of our competitors may use. Because of our investment in higher-quality ingredients and our focus on a “clean label”, we could have lower profit margins than some of our competitors if we are not able to establish a quality differentiator that resonates with consumers. Our sales may be particularly impacted as competitors increasingly emphasize lower-cost menu options.

Changes in consumer preferences or discretionary consumer spending could adversely impact our results.

Changes in consumer preferences and trends (for example, changes in consumer perceptions of certain ingredients that could cause consumers to avoid pizza or some of its ingredients in favor of foods that are or are perceived as healthier, lower-calorie, or lower in carbohydrate or otherwise based on their ingredients or nutritional content). Preferences for a dining experience such as fast casual pizza concepts, could also adversely affect our restaurant business and reduce the effectiveness of our marketing and technology initiatives. Also, our success depends to a significant extent on numerous factors affecting consumer confidence and discretionary consumer income and spending, such as general economic conditions, customer sentiment and the level of employment. Any factors that could cause consumers to spend less on food or shift to lower-priced products could reduce sales or inhibit our ability to maintain or increase pricing, which could adversely affect our operating results.

Food safety and quality concerns may negatively impact our business and profitability.

Incidents or reports of food- or water-borne illness or other food safety issues, investigations or other actions by food safety regulators, food contamination or tampering, employee hygiene and cleanliness failures, improper franchisee or employee conduct, or presence of communicable disease at our restaurants (Company-owned and franchised), QC Centers, or suppliers could lead to product liability or other claims. If we were to experience any such incidents or reports, our

15

brand and reputation could be negatively impacted. This could result in a significant decrease in customer traffic and could negatively impact our revenues and profits. Similar incidents or reports occurring at quick service restaurants unrelated to us could likewise create negative publicity, which could negatively impact consumer behavior towards us.

We rely on our domestic and international suppliers, as do our franchisees, to provide quality ingredients and to comply with applicable laws and industry standards. A failure of one of our domestic or international suppliers to meet our quality standards, or meet domestic or international food industry standards, could result in a disruption in our supply chain and negatively impact our brand and our results.

Failure to preserve the value and relevance of our brand could have a negative impact on our financial results.

Our results depend upon our ability to differentiate our brand and our reputation for quality. Damage to our brand or reputation could negatively impact our business and financial results. Our brand has been highly rated in U.S. surveys, and we strive to build the value of our brand as we develop international markets. As we experienced in 2018, the value of our brand and demand for our products could be damaged by any incidents that harm consumer perceptions of the Company, including negative publicity and consumer sentiment.

To be successful in the future, we must work to overcome the negative publicity we experienced in 2018, and preserve, enhance and leverage the value of our brand. Consumer perceptions of our brand are affected by a variety of factors, such as the nutritional content and preparation of our food, the quality of the ingredients we use, our corporate culture, our policies and systems related to diversity, equity and inclusion, our business practices and the manner in which we source the commodities we use. Consumer acceptance of our offerings is subject to change for a variety of reasons, and some changes can occur rapidly. Consumer perceptions may also be affected by third parties presenting or promoting adverse commentary or portrayals of our industry, our brand, our suppliers or our franchisees. If we are unsuccessful in managing incidents that erode consumer trust or confidence, particularly if such incidents receive considerable publicity or result in litigation, our brand value and financial results could be negatively impacted.

Our inability or failure to recognize, respond to and effectively manage the accelerated impact of social media could adversely impact our business.

In recent years, there has been a marked increase in the use of social media platforms, including blogs, chat platforms, social media websites, and other forms of internet-based communications that allow individuals access to a broad audience of consumers and other persons. The rising popularity of social media and other consumer-oriented technologies has increased the speed and accessibility of information dissemination. The dissemination of negative information via social media could harm our business, brand, reputation, marketing partners, financial condition, and results of operations, regardless of the information’s accuracy.

In addition, we frequently use social media to communicate with consumers and the public in general. Failure to use social media effectively could lead to a decline in brand value and revenue. Other risks associated with the use of social media include improper disclosure of proprietary information, negative comments about our brand, exposure of personally identifiable information, fraud, hoaxes or malicious dissemination of false information.

We may not be able to effectively market our products or maintain key marketing partnerships.

The success of our business depends on the effectiveness of our marketing and promotional plans, and in particular on the success of our efforts to relaunch our brand following the negative publicity we experienced in 2018. We may not be able to effectively execute our national or local marketing plans, particularly if lower sales continue to result in reduced levels of marketing funds. Additionally, our recent launch of an enhanced rewards program to help increase sales may not meet our expectations and could lower profitability. Our marketing strategy historically centered around the Company’s founder as brand spokesperson, and Mr. Schnatter’s removal as brand spokesperson in 2018 created the need for a new marketing strategy. We have also historically utilized relationships with well-known sporting events, professional teams and certain universities to market our products. The negative publicity we experienced in 2018 caused the loss of certain sports and university partnerships, and our business could continue to suffer if we are not able to create a compelling marketing

16

strategy, or maintain or grow key marketing relationships and sponsorships, or if we are unable to do so at a reasonable cost.

Our business will continue to require additional investments in alternative marketing strategies to address the challenges we faced in 2018. In 2018, we engaged a new advertising agency and introduced a new advertising campaign to focus the consumer’s attention on the core values of our brand. We expect to continue to invest in marketing to support the relaunch of our brand. If these efforts are not effective in increasing sales, we may be required to expend additional funds to effectively improve consumer sentiment and sales, and we may also be required to engage in additional activities to retain customers or attract new customers to the brand. Such marketing expenses and promotional activities, which could include discounting our products, could adversely impact our results.

Persons or marketing partners who endorse our products could take actions that harm their reputations, which could also cause harm to our brand. From time to time, in response to changes in the business environment and the audience share of marketing channels, we expect to reallocate marketing resources across social media and other channels. That reallocation may not be effective or as successful as the marketing and advertising allocations of our competitors, which could negatively impact the amount and timing of our revenues.

Our franchise business model presents a number of risks.

Our success increasingly relies on the financial success and cooperation of our franchisees, yet we have limited influence over their operations. Our franchisees manage their businesses independently, and therefore are responsible for the day-to-day operation of their restaurants. The revenues we realize from franchised restaurants are largely dependent on the ability of our franchisees to grow their sales. If our franchisees do not experience sales growth, our revenues and margins could be negatively affected as a result. Also, if sales trends worsen for franchisees, especially in emerging markets and/or high cost markets, their financial results may deteriorate, which could result in, among other things, higher levels of required financial support from us, higher numbers of restaurant closures, reduced numbers of restaurant openings, delayed or reduced payments to us, or increased franchisee assistance, which reduces our revenues.

Our success also increasingly depends on the willingness and ability of our franchisees to remain aligned with us on operating, promotional and marketing plans. Franchisees’ ability to continue to grow is also dependent in large part on the availability of franchisee funding at reasonable interest rates and may be negatively impacted by the financial markets in general or by the creditworthiness of our franchisees. Our operating performance could also be negatively affected if our franchisees experience food safety or other operational problems or project an image inconsistent with our brand and values, particularly if our contractual and other rights and remedies are limited, costly to exercise or subjected to litigation. If franchisees do not successfully operate restaurants in a manner consistent with our required standards, the brand’s image and reputation could be harmed, which in turn could hurt our business and operating results.

The issuance of shares of our Series B Preferred Stock to Starboard and its permitted transferees dilutes the ownership and relative voting power of holders of our common stock and may adversely affect the market price of our common stock.

Pursuant to a Securities Purchase Agreement (the “Securities Purchase Agreement”) among the Company and certain funds affiliated with or managed by Starboard Value LP (“Starboard”), the Company sold 200,000 shares of our newly designated Series B Convertible Preferred Stock, par value $0.01 per share (the “Series B Preferred Stock”) to Starboard on February 3, 2019 (the “Closing”), with Starboard having the option to purchase up to an additional 50,000 shares of Series B Preferred Stock on or prior to March 29, 2019.

The initial shares sold to Starboard at the Closing represent approximately 11% of our outstanding common stock on an as-converted basis, and would represent in the aggregate an estimated 14% of our outstanding common stock on an as-converted basis assuming Starboard exercised in full their option to purchase an additional 50,000 shares of Series B Preferred Stock. The Series B Preferred Stock is convertible at the option of the holders at any time into shares of common stock based on the conversion rate determined by dividing $1,000, the stated value of the Series B Preferred Stock, by $50.06.

17

Because holders of our Series B Preferred Stock are entitled to vote, on an as-converted basis, together with holders of our common stock on all matters submitted to a vote of the holders of our common stock, the issuance of the Series B Preferred Stock to Starboard effectively reduces the relative voting power of the holders of our common stock.

In addition, the conversion of the Series B Preferred Stock into common stock would dilute the ownership interest of existing holders of our common stock. Furthermore, following expiration of Starboard’s one-year lock-up period, any sales in the public market of the common stock issuable upon conversion of the Series B Preferred Stock could adversely affect prevailing market prices of our common stock. We granted Starboard customary registration rights in respect of their shares of Series B Preferred Stock and any shares of common stock issued upon conversion of the Series B Preferred Stock. These registration rights would facilitate the resale of such securities into the public market, and any such resale would increase the number of shares of our common stock available for public trading. Sales by Starboard of a substantial number of shares of our common stock in the public market, or the perception that such sales might occur, could have a material adverse effect on the price of our common stock.

Our Series B Preferred Stock has rights, preferences and privileges that are not held by, and are preferential to, the rights of our common stockholders, which could adversely affect our liquidity and financial condition, result in the interests of Starboard differing from those of our common stockholders and delay or prevent an attempt to take over the Company.

Starboard, as the holder of our Series B Preferred Stock, has a liquidation preference entitling it to be paid, before any payment may be made to holders of our common stock in connection with a liquidation event, an amount per share of Series B Preferred Stock equal to the greater of (i) the stated value thereof plus accrued and unpaid dividends and (ii) the amount that would have been received had such share of Series B Preferred Stock been converted into common stock immediately prior to such liquidation event.